Overview of New NISA Users as of January 2026

More than two years have passed since the revised NISA (hereafter " New NISA"), introduced in 2024, began.

As of the end of December 2025, the number of NISA accounts stood at approximately 28.26 million1, an increase of about 2.67 million accounts compared with the same month the previous year.

This article mainly presents the situation based on a questionnaire conducted by the Japan Securities Dealers Association (JSDA), which collected responses in January 2026 from 7,926 people who purchased financial products with the New NISA in 20252.

1JSDA, “Status of NISA Account Openings and Use (as of end-December 2025) [Preliminary Report]”

2JSDA, “Survey on Usage Trends after the Start of the New NISA (Summary of Survey Results)”

Attributes

First, respondent attributes.

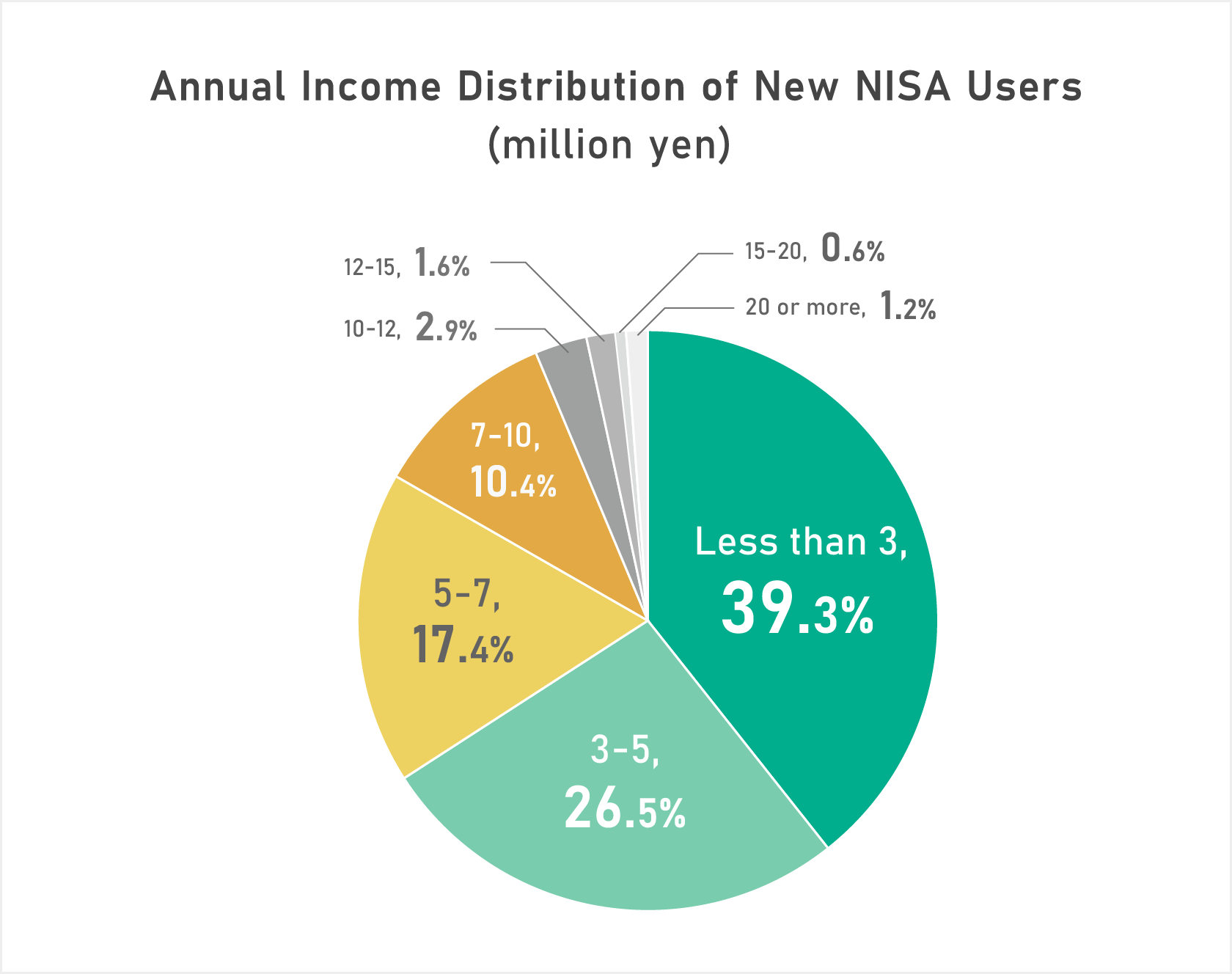

Looking at income distribution, 39.3% of respondents have annual incomes under ¥3 million, and 26.5% have incomes between ¥3 million and under ¥5 million. These two income brackets alone account for 65.8% of respondents, indicating that NISA is being used across a wide range of income levels.

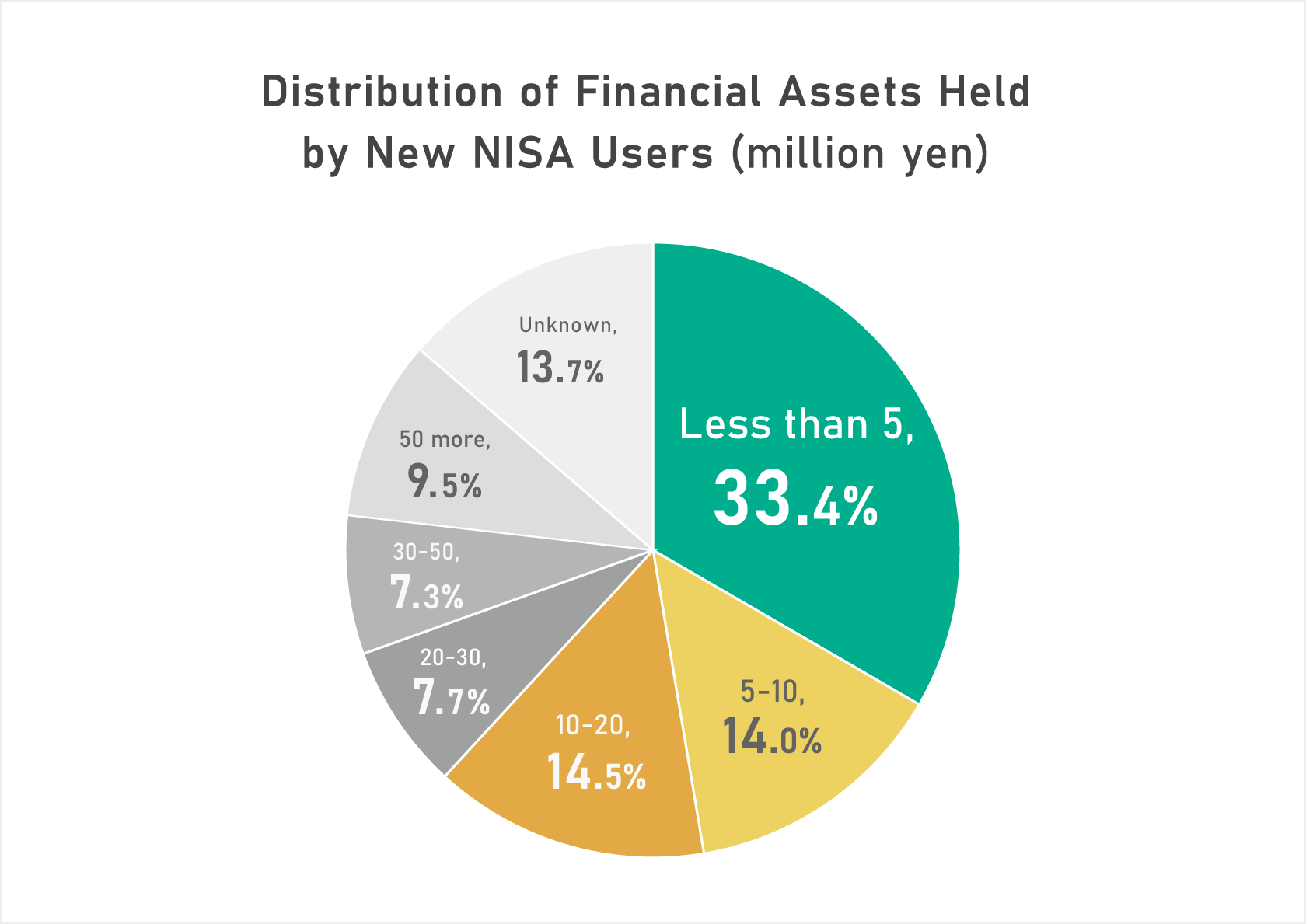

Next, let’s look at amounts of financial assets held.

About one-third (33.4%) of respondents hold less than ¥5 million in financial assets, which also suggests that users are not especially concentrated among wealthy individuals.

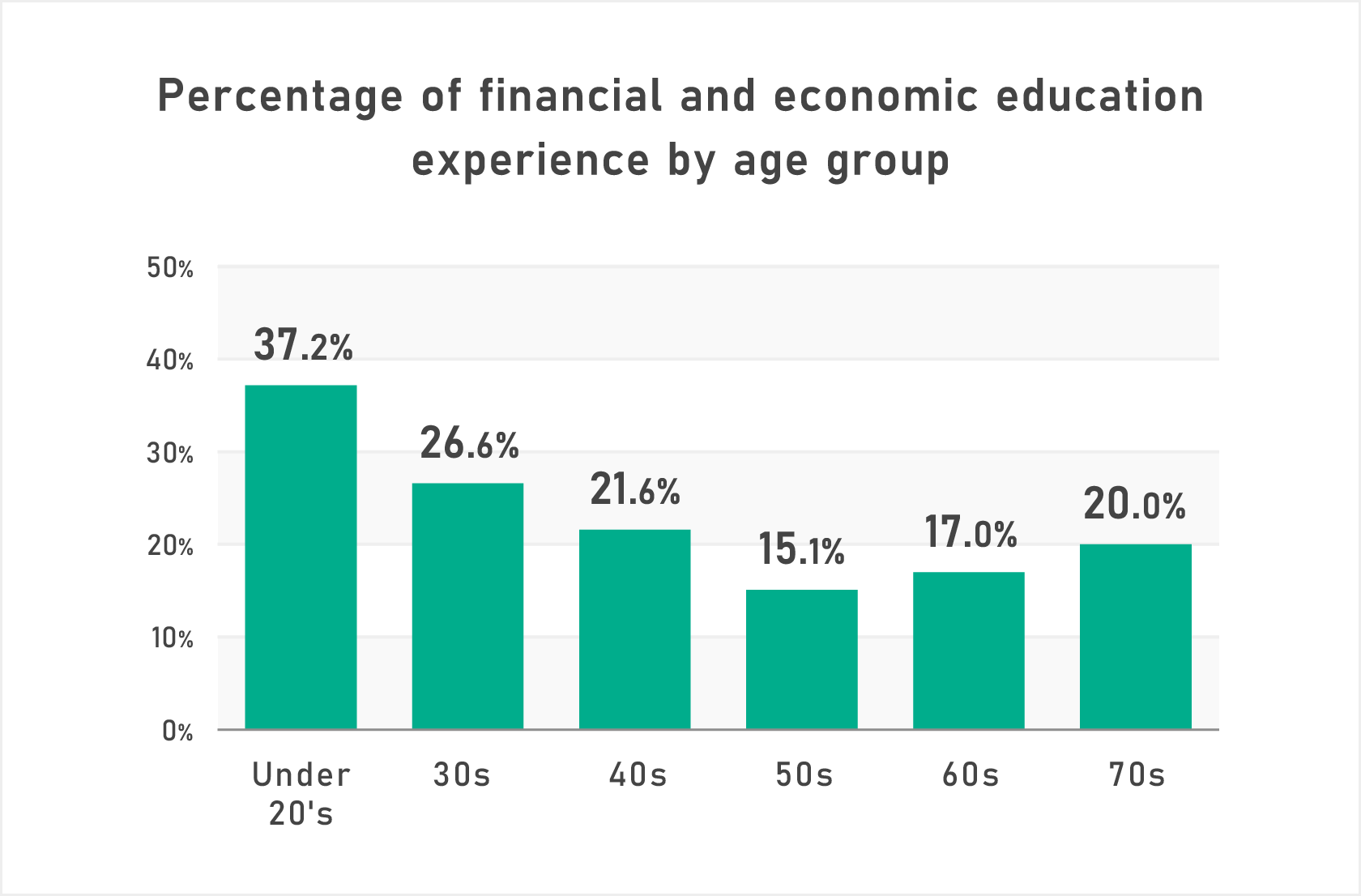

Now consider experience with financial and economic education.

Overall, 22.7% of respondents reported having such education experience. Conversely, 77% of new NISA users started using the system without experience in financial and economic education.

Below is the breakdown by age group. Younger people tend to have higher rates of financial and economic education participation.

Purchased Securities and Selling Behavior

What kinds of securities are respondents buying in their New NISA accounts?

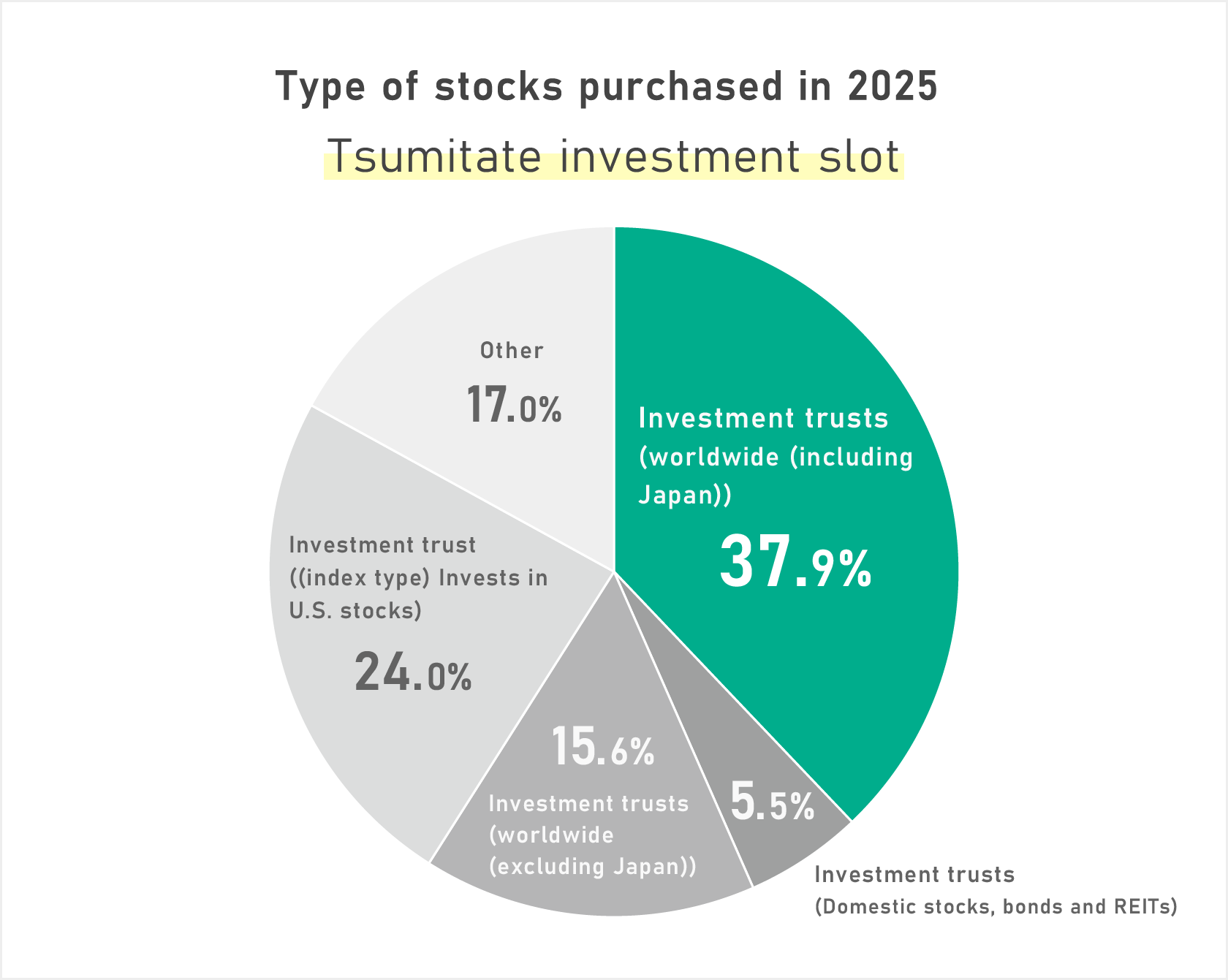

First, the Tsumitate (regular savings) investment slot.

As shown below, 37.9% of holdings in this slot are investment trusts investing in global equities including Japan.

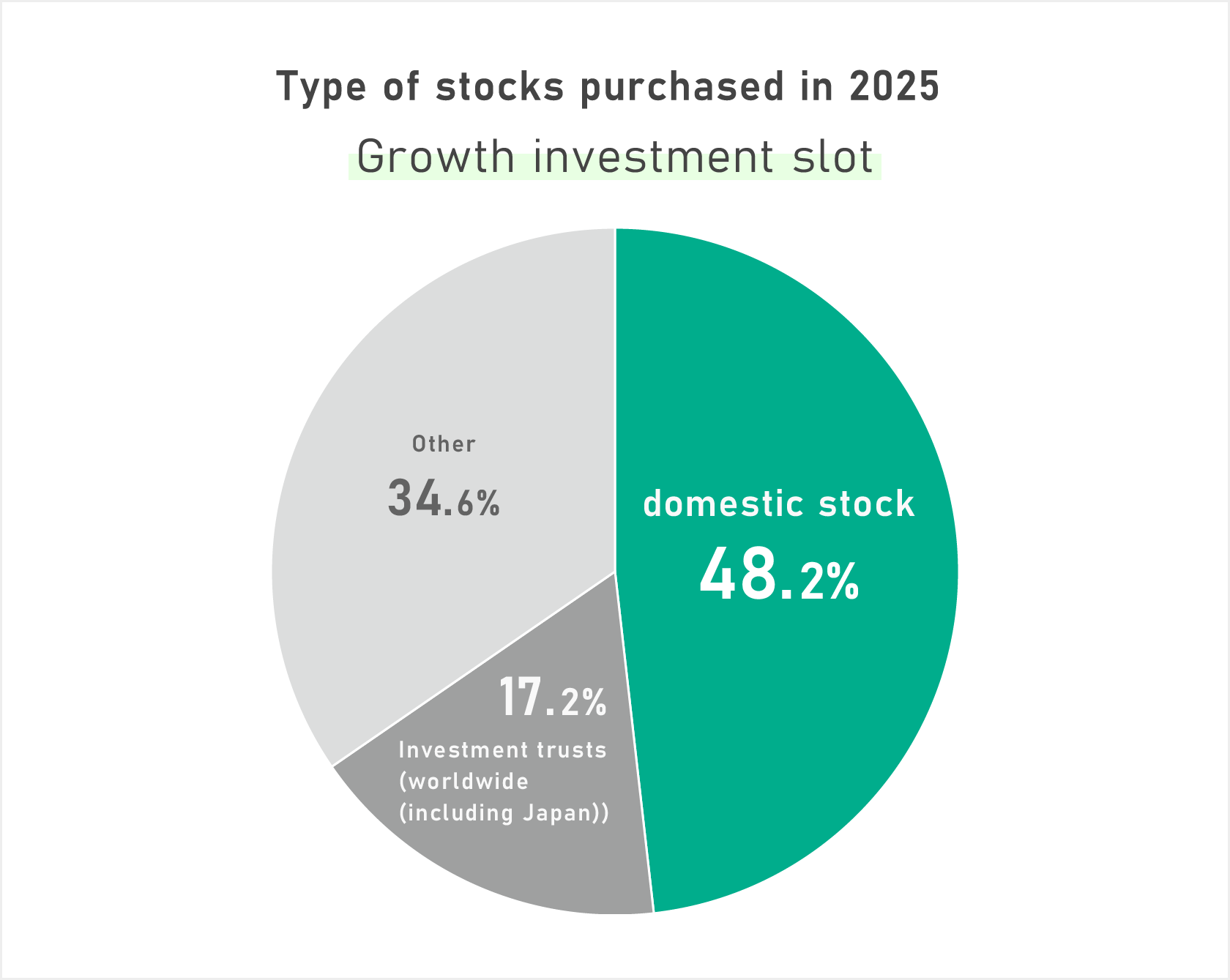

The Growth investment slot

In the Growth investment slot, domestic equities account for nearly half (48.2%), showing a different pattern from the Tsumitate investment slot.

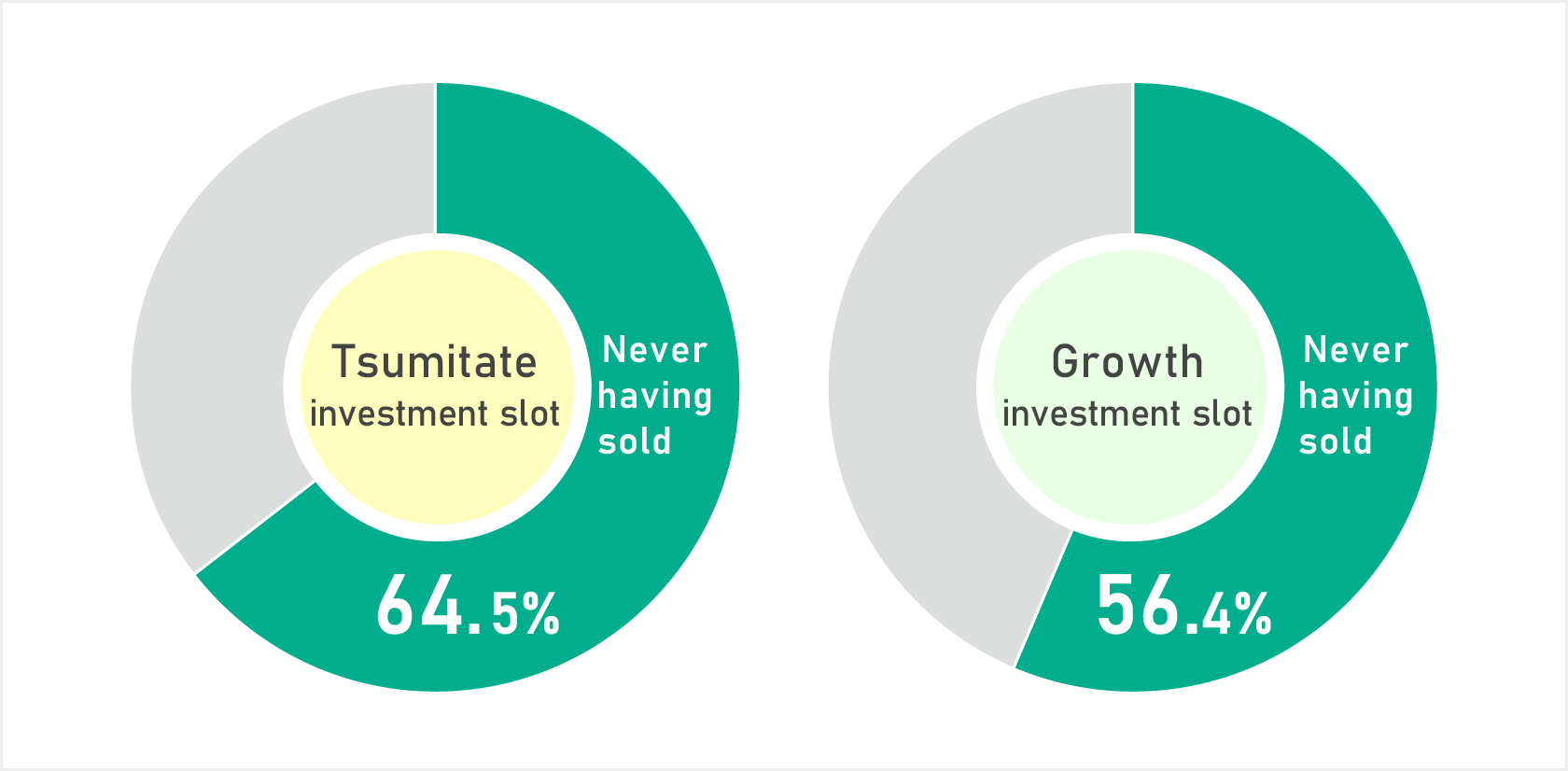

Selling behavior

With two years having passed since the new system began and markets performing well, the proportion of people who sold increased from last year. Nonetheless, reflecting the focus on long-term investing that is central to NISA, a majority in both slots reported never having sold: 64.5% in the Tsumitate investment slot (vs. 83.2% last year) and 56.4% in the Growth investment slot (vs. 75.3% last year).

Profit and Loss Status

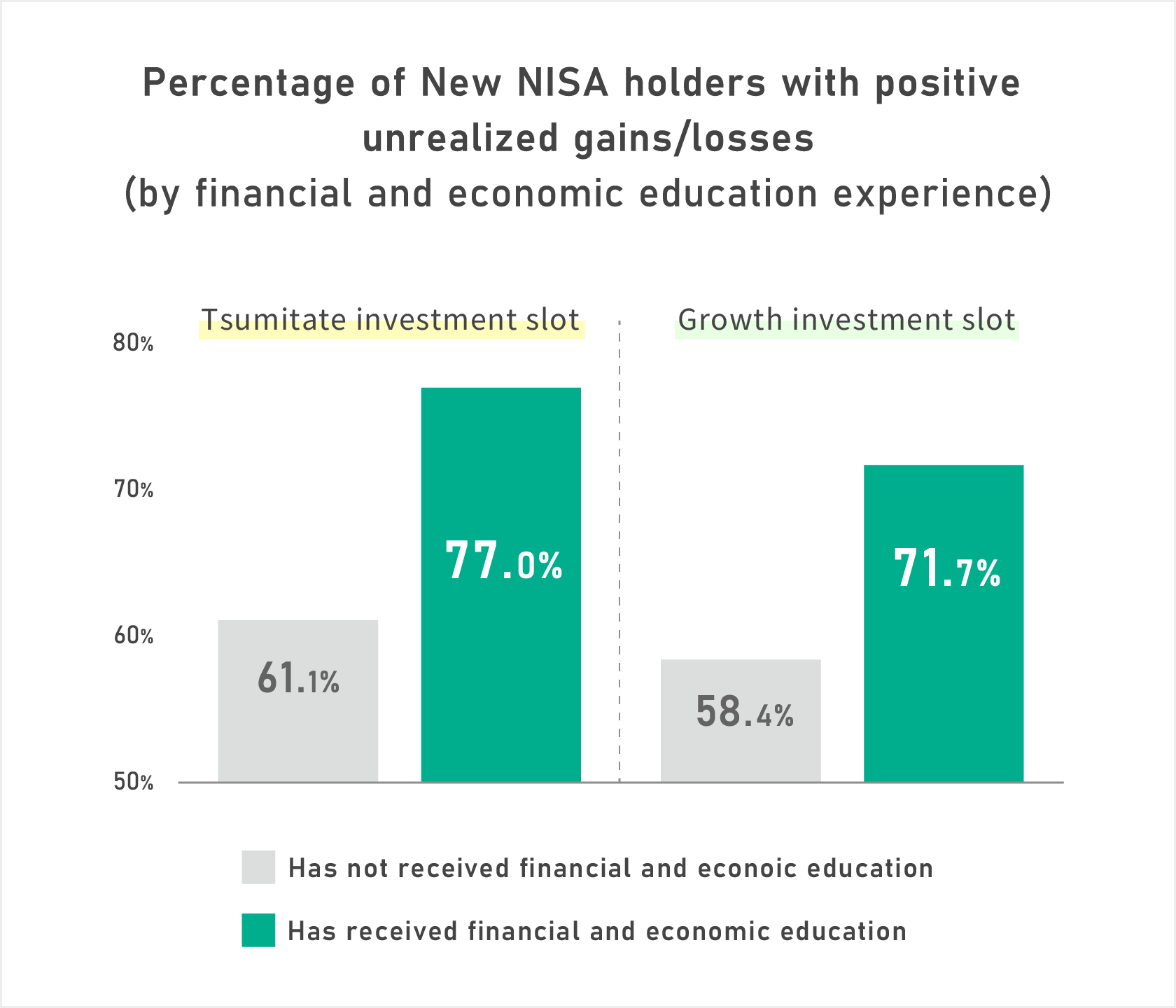

Finally, let’s look at unrealized profit and loss in New NISA accounts.

In the Tsumitate investment slot, 64.9% reported being in positive territory, and in the Growth investment slot 61.7% reported being positive. The share reporting negative positions was only 1.6% for the Tsumitate investment slot and 4.0% for the Growth investment slot.

Dividing those reporting unrealized gains by whether they had financial and economic education yields the following results.

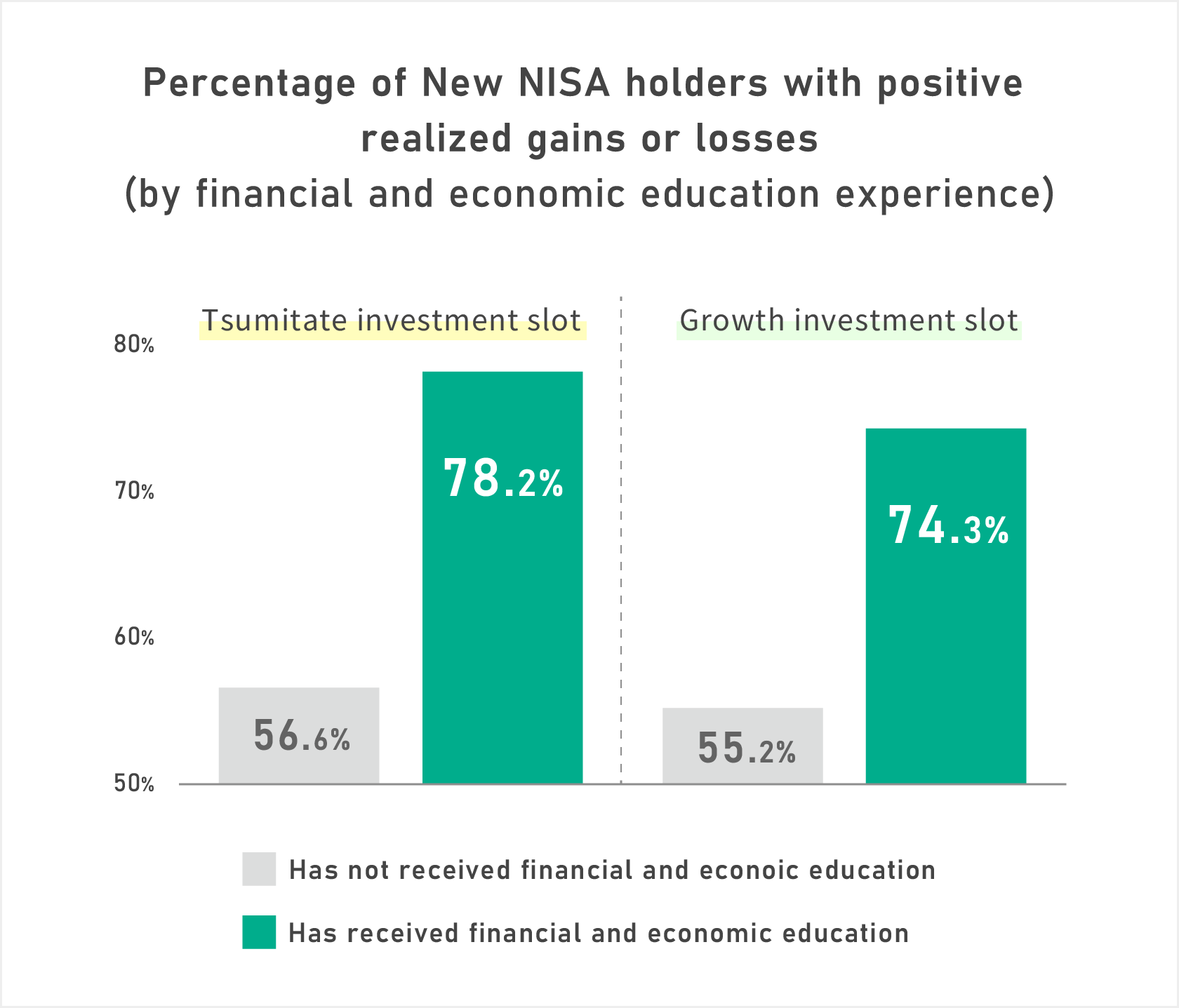

Realized profit and loss shows a similar trend to unrealized profit and loss.

In the Tsumitate investment slot, 63.9% reported realized gains, and in the Growth investment slot 60.9% reported realized gains. The proportions reporting realized losses were 2.8% for the Tsumitate investment slot and 4.7% for the Growth investment slot.

Splitting those with realized gains by financial and economic education experience produces the following results.

As shown, those who have received financial and economic education are relatively more likely to report positive profit and loss than those without such experience.

Intention to Use the Children's NISA System

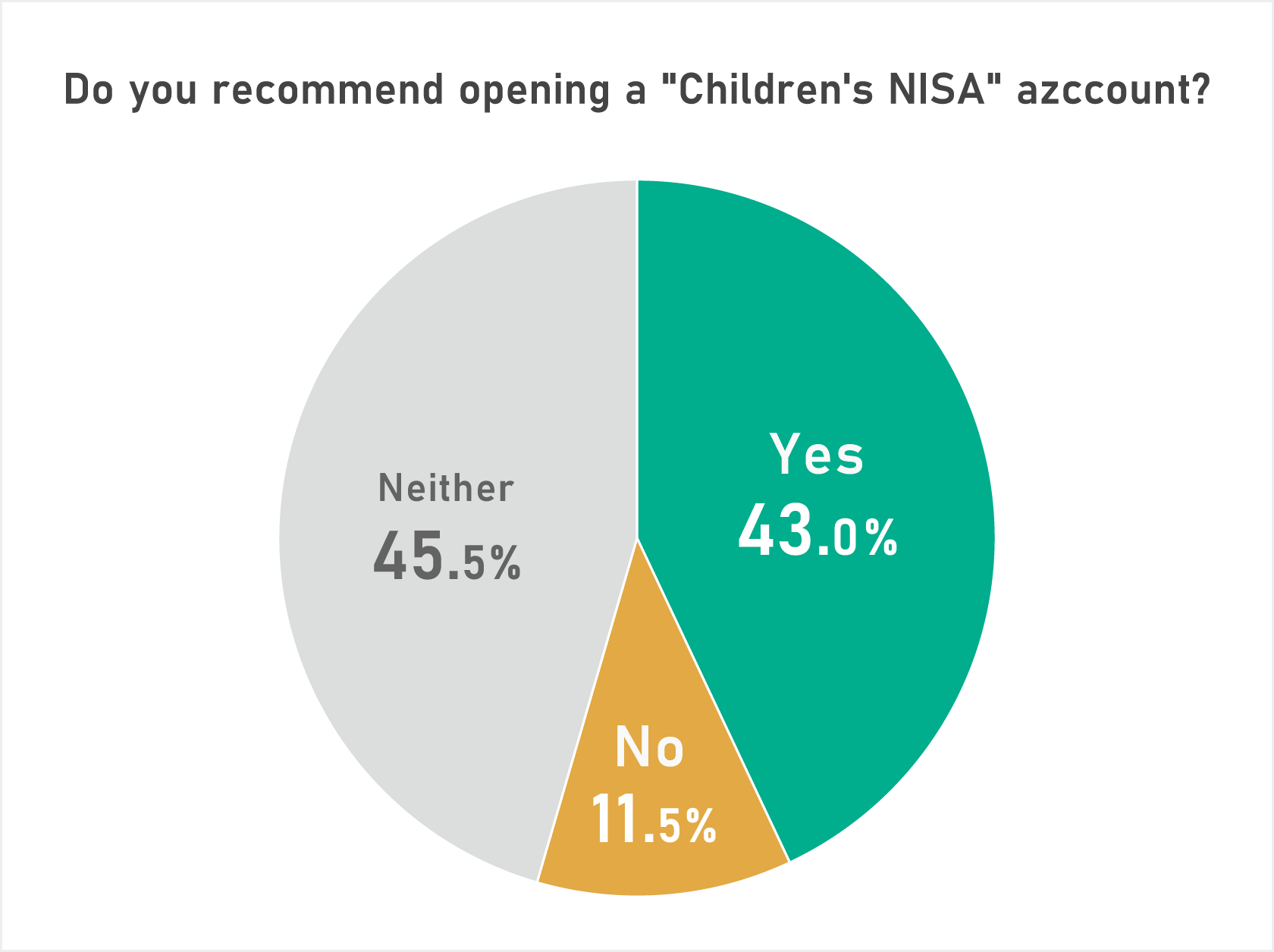

Finally, regarding intentions toward the so-called “Children’s NISA,” which will start in 2027.

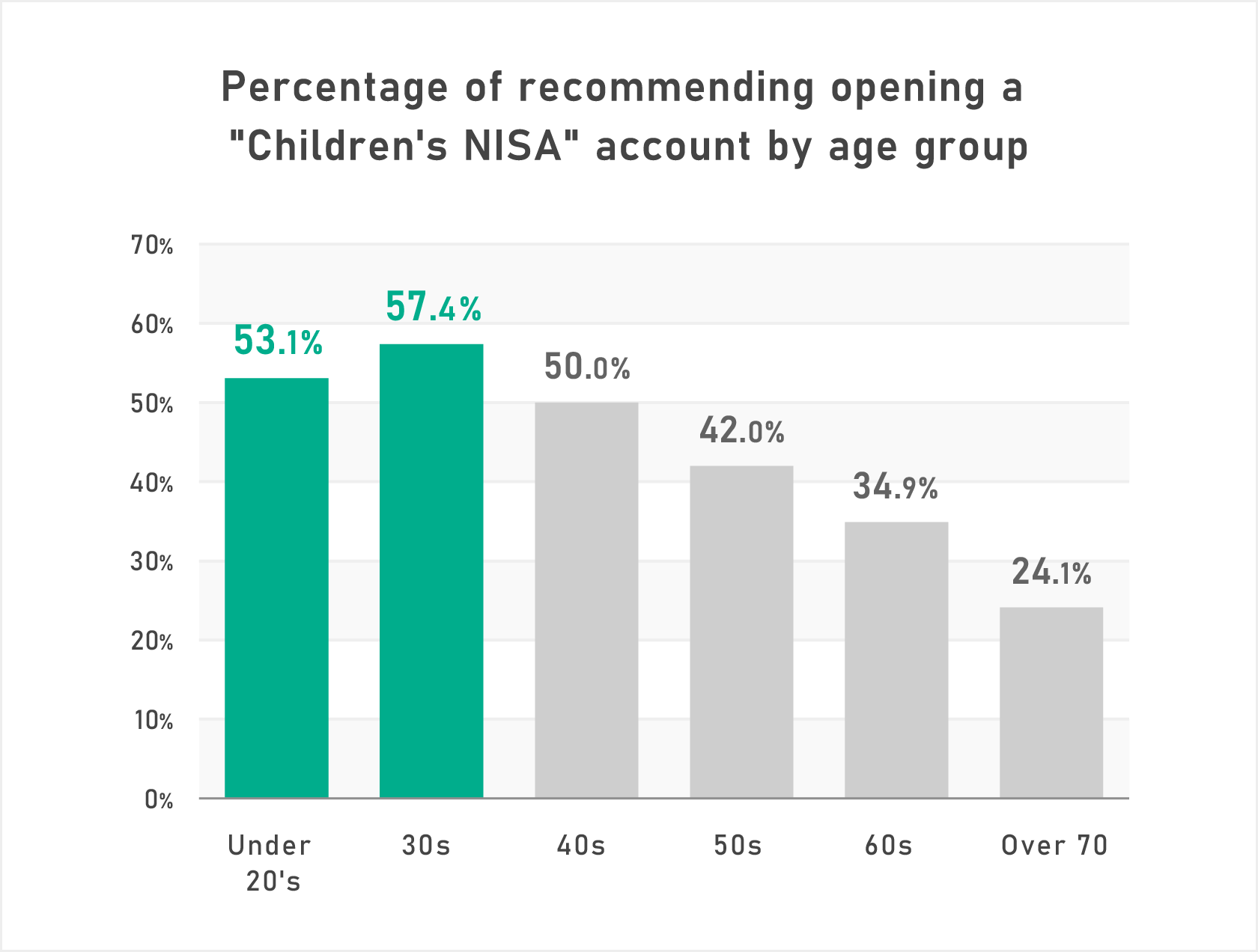

Among respondents who have children or grandchildren, 43% said they would “Recommend it,” while only 11.5% answered they would “not Recommend it,” and the remaining 45.5% answered “neither.” The relatively high share of “neither” responses may be partly because the survey was conducted January 14–16, 2026, a time when detailed information about the program and ways to use it was still limited.

Looking at responses by age, recommendation rates are in the 50% range among people in their 20s to 40s, peaking in the 30s and gradually declining thereafter, suggesting the program has support among those with relatively young children.

As shown above, New NISA users come from a wide range of incomes and asset holdings, and most have not received financial and economic education.

However, since those with financial and economic education tend to show higher proportions of positive returns, learning while managing assets may lead to better asset formation.

Author: Daisuke Yabuuchi, Financial Well-Being Department, Nomura Holdings, Inc.

This document was prepared by Nomura Securities Co., Ltd. based on data judged reliable as of April 2026 and does not guarantee accuracy or completeness. Information may change in the future. All rights to any part of this material belong to Nomura Securities Co., Ltd., and no part may be reproduced or transmitted in any form or by any means, electronic or mechanical, for any purpose without prior permission.

Published in English: May 13, 2026

Original publication date: March 13, 2026

関連記事